To keep the “affordable” in the Affordable Care Act, Silver Plans purchased through the Healthcare Marketplace come with financial assistance for low and moderate-income consumers.

These “extra savings” help consumers afford their monthly premiums. They also reduce the co-pay amounts paid to healthcare providers and for prescription drugs. Annual deductibles and co-insurance costs are also lower.

You may qualify for these savings if your household income is between 12,000 to $30,000 for an individual, or about $24,000 to $60,750 for a family of four.

The savings can be substantial if you have substantial healthcare needs or require many medications.

An analysis by the Commonwealth Fund gives this example: “Someone earning $17,000 who is also a high user of care, projected out-of-pocket spending would be no higher than $650—a savings of nearly $6,000 compared to the average silver plan. In other words, instead of potentially spending more than a third of his income on health care expenses, he spends no more than 3.8 percent of his income…”

Without premium subsidies and share-of-costs savings, many consumers would not be able to afford their health insurance. In 2017, 7 million people qualified for this assistance -—58 percent of all marketplace enrollees.

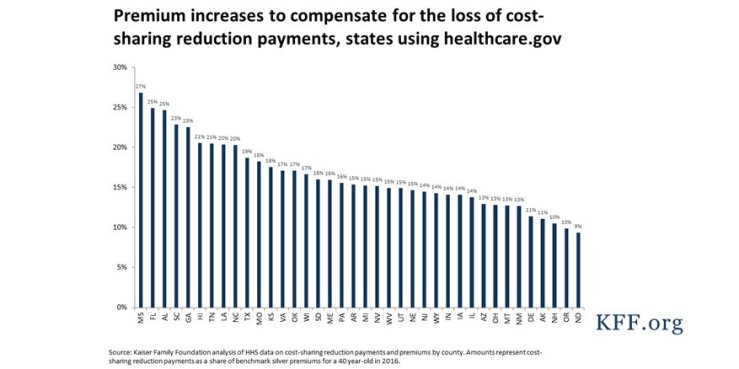

If these savings were eliminated, as proposed in some reform plans being considered, insurance costs would rise, as insurance companies would be forced to increase premiums. Some Silver Plan premiums could increase by 9 to 27 percent, according to some reports. And out-of-pocket costs would also increase. In Florida, the Kaiser Family Foundation predicts premiums could increase 25 percent if the share-of-costs savings are eliminated.

You find out if you qualify for premium tax credits and these extra savings when you fill out your marketplace application through healthcare.gov. More information is available here: https://www.healthcare.gov/lower-costs/save-on-out-of-pocket-costs/

· Frequently asked questions:

What is a copayment or coinsurance? Payments you make each time you get care – like $30 for a doctor visit. The extra savings could mean you pay $20 or $15 instead.

Do these extra savings apply to my “out-of-pocket maximum?” Yes. If you incur high costs in one year because you become seriously ill or had an accident, you are protected with a maximum amount. The extra savings also help lower this amount.

Source: Essential Facts About Health Reform Alternatives: Eliminating Cost-Sharing Reductions, The Commonwealth Fund, April 2017